Wealthfront's IPO: Betting on Execution Excellence or Betting Against AI Disruption?

A comprehensive analysis of proven performance, strategic positioning, and existential transformation risk

The Real Story Behind the UBS Deal That Never Was

When UBS walked away from its $1.4 billion acquisition of Wealthfront in September 2022, the headlines masked a more nuanced reality. As detailed in my 2022 analysis, Ironic is the only word to describe Wealthfront`s fate, the "$1.4B" figure was misleading; only around $700 million was cash upon closing, with the remainder contingent on performance milestones that were never disclosed. This structure made the deal far more comparable to Personal Capital's $1 billion acquisition by Empower Retirement (roughly 10x revenues) than the eye-popping multiples initially reported.

The deal's collapse wasn't simply a matter of market conditions. Naureen Hassan, UBS's new president of Americas (formerly the architect of Schwab's Intelligent Portfolios), likely orchestrated the termination after recognizing that integration, not acquisition, was the key to unlocking value in digital wealth management. As I wrote in 2022: "Hassan knows very well how cultural conflicts can wipe out the value of any such acquisition and has therefore made this choice to work on a clean sheet."

The irony remains striking: Wealthfront, once the poster child for "Self-driving Money," had already compromised its low-cost principles by launching the actively managed Wealthfront Risk Parity Fund (WFRPX) in 2018, a move that generated $1.3 billion in AUM despite dismal performance. This cultural drift likely factored into UBS's decision to pay an estimated $300 million termination fee rather than proceed with a potentially value-destructive integration.

Is Wealthfront Still an Innovator?

The fundamental question for IPO investors today is whether Wealthfront remains an innovator or has become just another financial services company chasing growth through traditional tactics.

Evidence of diminished innovation, losing strategic focus, and drifting away from its founding purpose:

Banking pivot: Like every fintech, Wealthfront transitioned into cash accounts and banking services through its partnership with Green Dot, precisely what I predicted in 2022 as "the traditional tactics of new banking entrants."

Trading features: Added DIY trading capabilities "à la Robinhood"

Complex products: The WFRPX fund represents everything Wealthfront originally stood against

Incremental improvements: Recent features like fractional S&P 500 investing, while useful, are table stakes rather than breakthrough innovations

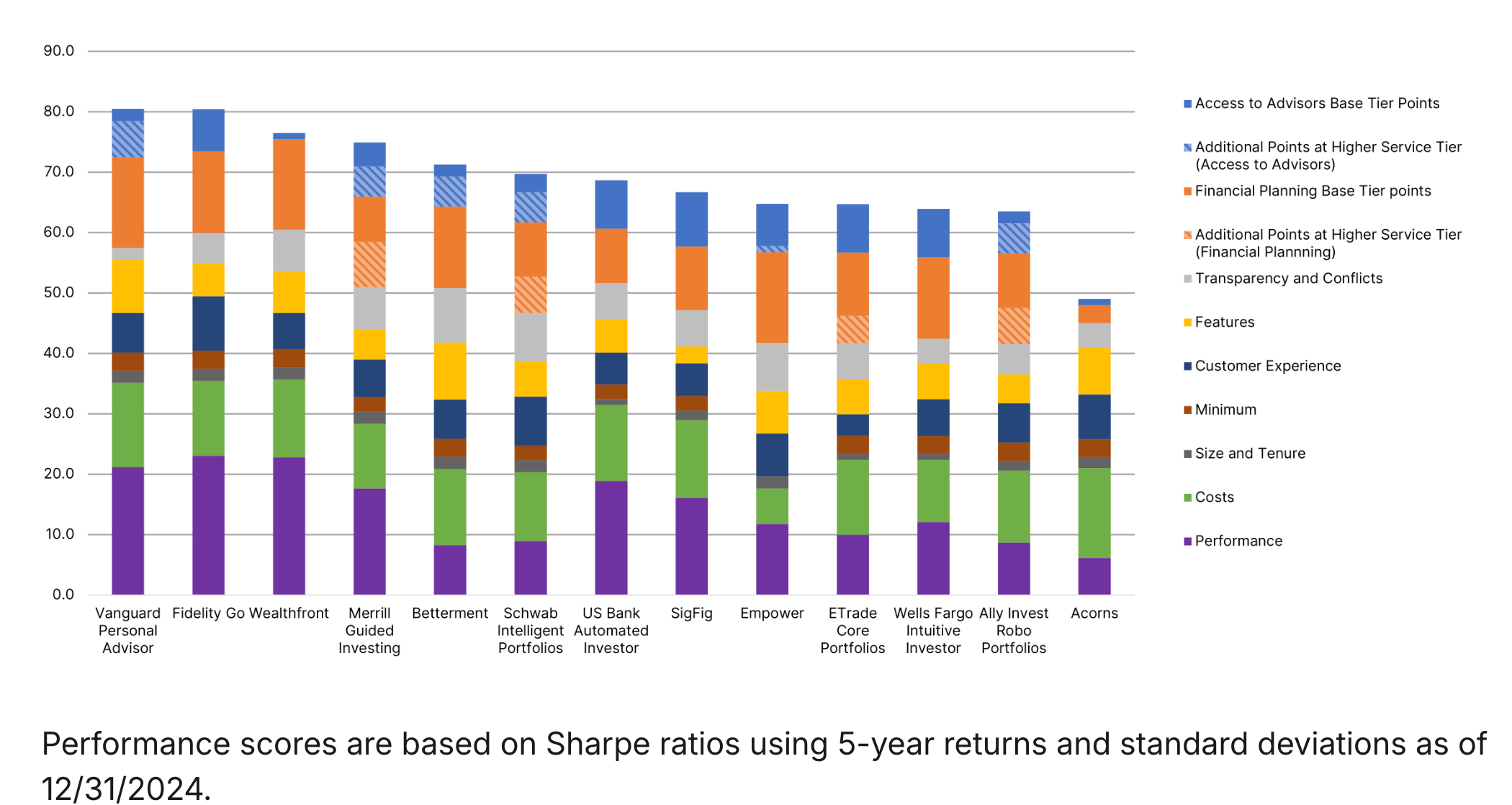

However, recent performance metrics indicate a comeback in execution excellence compared to the competition, both from incumbents and Fintechs. Condor Capital's Q1 2025 robo-advisor rankings awarded Wealthfront the "Best Robo for Performance at a Low Cost," citing its dedicated energy holdings, competitive fees, and robust returns. In Condor's comprehensive analysis of major platforms, including Vanguard, Fidelity, Betterment, and Schwab, Wealthfront scored highest on performance metrics while maintaining a cost leadership position.

Recent innovation in direct indexing: Wealthfront has also revitalized its direct indexing offering, launching a 9-basis-point S&P 500 direct indexing portfolio with a $20,000 minimum (down from $100,000), undercutting Schwab's 40-basis-point fee and $100,000 minimum. This positions Wealthfront competitively in the direct indexing market, projected to reach $825 billion by 2026 (Source).

This recognition and product innovation suggest that while Wealthfront may not be pioneering entirely new categories, it's executing better than competitors on the fundamentals that matter most to investors: returns, costs, and accessible innovation.

The innovation question matters more than ever, because:

Robo-advisory has matured into a commodity

Incumbents like Vanguard ($311B AUM) and Schwab ($81B AUM) now dominate with similar automated offerings

True differentiation may now come from execution excellence rather than feature innovation

The Mystery of Wealthfront's Growth Surge

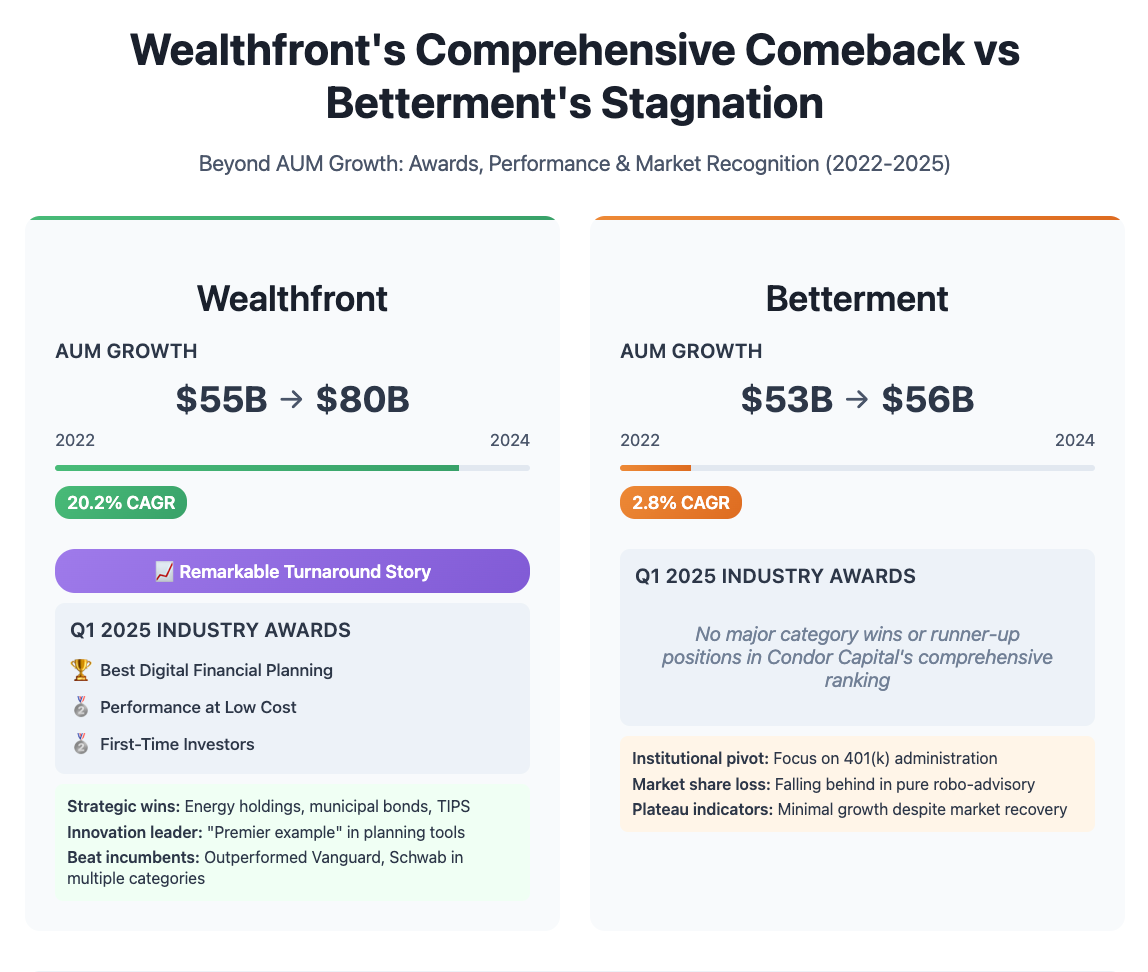

Perhaps the most surprising development since 2022 has been Wealthfront's remarkable growth acceleration (something I didn’t expect when doing this research). Data from RIABiz (as of end of 2024) reveals the accurate scale of this transformation: Wealthfront administered $75 billion in total assets ($37.4B investments + $37.6B cash), compared to 2023 totals of $31 billion ($23B investments + $8B cash), representing 63% investment growth and 370% cash growth year-over-year.

This comprehensive growth (latest figures are $80 billion in assets) extends beyond AUM to total client relationships: Wealthfront now serves over 1 million total clients (386,212 investing clients + estimated 613,788 banking clients), demonstrating successful execution of the banking pivot from 2022.

Key growth drivers of this 2-year turnaround:

Banking integration success: Cash accounts exploded from $8B to $37.6B, validating the "traditional tactics of new banking entrants" strategy

Mass affluent capture: Average investing client balance of $93,000 with estimated $61,250 in affiliated bank accounts

Market recovery benefits: 63% investment AUM growth aided by favorable market conditions

Scale economics: Achieved profitability with 2023 EBITDA of $89 million

Most significantly for IPO investors: In December 2024, Wealthfront conducted an employee stock buyback at a $2 billion valuation, representing a 42% premium to the failed $1.4 billion UBS deal price, according to The Information. The company is projected to generate approximately $290 million in revenues and $100 million in free cash flow for 2024.

Why Comparisons with SoFi, Robinhood, and Others Miss the Mark

The analysis of Wealthfront's competitive position requires careful distinction between fundamentally different business models:

Why SoFi comparisons are misleading:

SoFi is primarily a lending platform (student loans, mortgages, personal loans) with investment services as a secondary offering

Their $36.25B AUM includes significant cross-selling from loan customers

Their revenue model depends heavily on interest income, not just management fees

Growth likely reflects broader platform adoption rather than pure investment service demand

Why Robinhood doesn't belong in this analysis:

Robinhood is a brokerage focused on active trading, not passive wealth management, even though they have added retirement offerings

Revenue is from PFOF (payment for order flow) and margin lending, not management fees

Customer behavior and retention patterns are fundamentally different

Their $193B AUM includes highly active, speculative accounts

Why Empower/Personal Capital operates in a different league:

Empower focuses on high-net-worth individuals and 401(k) administration

Their $200B AUM includes significant retirement plan assets

Human advisor hybrid model commands higher fees

Customer profile skews older and wealthier

The only valid comparison is Betterment. Both Wealthfront and Betterment operate pure-play robo-advisory models targeting similar demographics with comparable fee structures. This makes their divergent growth trajectories, Wealthfront's 20.2% CAGR vs. Betterment's 2.8% CAGR, a meaningful competitive indicator in favor of Wealthfront.

Condor Capital's Q1 2025 rankings provided additional context. While both platforms were analyzed alongside 10 other major robo-advisors, Wealthfront won the "Best Robo for Performance at a Low Cost" award, while Betterment ranked lower across key performance metrics. This suggests Wealthfront's growth advantage may reflect superior execution.

Wealthfront vs. Betterment: The Real Competitive Dynamic

The most telling comparison reveals Wealthfront's relative strength in the pure robo-advisory space. Honestly, I didn't expect such a significant divergence when I embarked on this research.

The two original Robo leaders have different strategic positioning. Wealthfront is focused on automation and tax optimization for individual investors, while Betterment has diversified into 401(k) administration and institutional services.

Betterment's institutional pivot has not only diluted its consumer focus but has also allowed Wealthfront to grow its market share in the core robo-advisory consumer segment.

However, neither has cracked the code on competing with incumbent robo-offerings from Vanguard and Schwab. Wealthfront's investment AUM ($37.4B) is still significantly below Schwab's robo-advisor AUM ($81B). However, if we count Wealthfront's total assets under administration ($80B), then they've essentially matched Schwab's robo-advisor offering.

Highlights from Condor Capital's Q1 2025 Robo Report

Condor Capital's comprehensive Q1 2025 Robo Report highlights that I've identified a way to strengthen Wealthfront's IPO investment thesis:

Innovation Vindication: The report positions Wealthfront as still innovative, particularly in planning tools

Performance Validation: Their investment strategy (energy, munis, TIPS) has delivered results, not just AUM growth

Digital Leadership: Recognition as a digital planning leader suggests they've maintained a technological edge despite the commoditization of these services. While robo-advisory investment management has become commoditized, Wealthfront has differentiated itself through superior digital planning capabilities, winning "Best Digital Financial Planning" against all competitors and being called a "premier example of innovation" for planning tools. This suggests they've successfully pivoted from just being a portfolio manager to becoming a comprehensive digital financial platform.

Positioning vs. Incumbents: Multiple category wins/runner-ups against Vanguard, Fidelity, and others validate competitive strength. Specifically, Wealthfront outperformed or matched industry giants across multiple categories, beating Vanguard in "Digital Financial Planning," coming second only to Fidelity Go in "Performance at Low Cost," and earning runner-up in "First-Time Investors" ahead of Schwab, Betterment, and others. This multi-category recognition across 12 major platforms, including the largest asset managers in the world, demonstrates that Wealthfront isn't just surviving but thriving against well-funded incumbents.

Target Market Clarity: Strong positioning for first-time investors and digital-native users supports my thesis about the younger demographic appeal

Remarkable Turnaround: Wealthfront appears to have emerged from its 2019-2022 stagnation period. The combination of AUM growth, multiple industry awards, and strong performance metrics suggests the company has successfully navigated both the failed UBS acquisition and the broader fintech downturn. This turnaround—from a company that was struggling to grow and compromising its principles (WFRPX fund) to an award-winning platform outperforming incumbents—represents a compelling comeback narrative for IPO investors.

This data from Condor Capital's analysis strengthens the case that Wealthfront's growth isn't just marketing-driven but reflects genuine product excellence and execution, key for IPO credibility.

The IPO: Strategic Choice or Market Timing?

Wealthfront's IPO filing represents either a comeback story or a company running out of options and trying to sustain its comeback. The 2022 UBS deal collapse, while potentially wise for UBS, left Wealthfront needing to prove it could thrive independently.

Wealthfront`s 2-year journey since then shows the following:

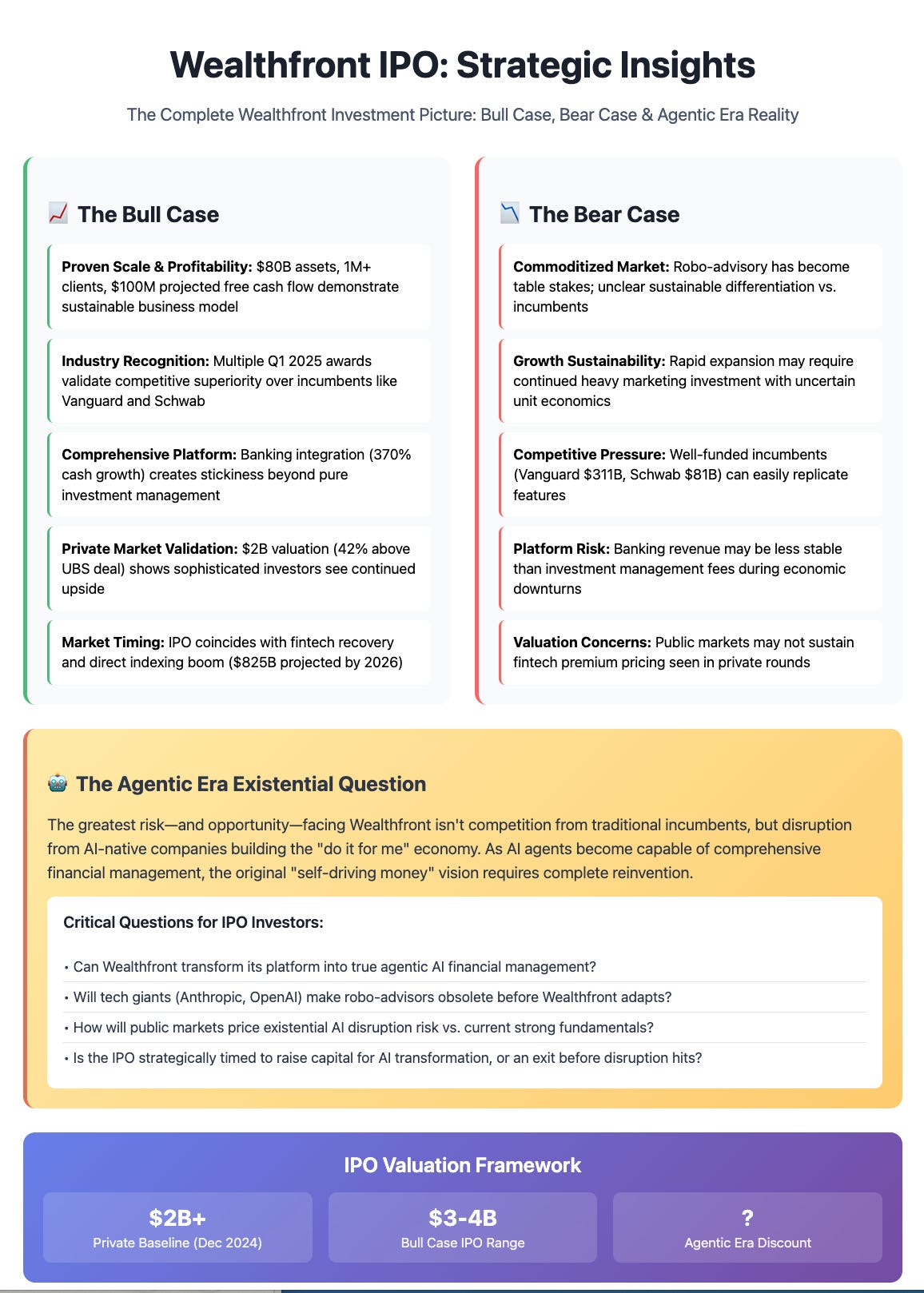

The bull case:

Sustained AUM growth demonstrates product-market fit

Younger customer base represents long-term value as wealth accumulates

Banking integration creates stickiness and cross-selling opportunities

IPO timing coincides with fintech market recovery

The bear case:

Growth may be unsustainable without continued marketing investment

Competitive moat remains unclear against better-funded incumbents

Path to profitability still uncertain despite scale

Innovation and the company's founding vision necessitate a comprehensive AI-powered transformation that fundamentally alters the business at its core.

The real test: Can Wealthfront demonstrate that it's more than just a smaller, purer version of what Vanguard and Schwab now offer? In my opinion, unless they design and execute on a roadmap that redefines self-driving money (their original vision) in the AI-era, Wealthfront and many other Fintechs are at risk of eventual extinction. The IPO filing will need to articulate not just growth metrics and execution excellence, but a compelling vision for survival in an AI-dominated financial landscape where tech giants (Claude and Perplexity for finance, etc) are building the ultimate 'Do it for me' economy.

The Agentic Era Challenge: Can Self-Driving Money Survive AI Disruption?

Wealthfront's IPO represents more than just another fintech listing; it's a test of whether the original robo-advisory vision can survive and thrive in a world where that innovation has been commoditized by incumbents, the Agentic economy is upon us, and the disruptor AI leaders are launching financial services.

The company's journey from near acquisition to IPO candidacy reflects broader tensions in fintech: the challenge of maintaining innovation while scaling, the difficulty of competing with well-funded incumbents, the pressure to expand beyond core competencies, and the major challenge of transforming into the Agentic era.

Condor Capital's analysis suggests Wealthfront has successfully navigated some of these challenges (except the Agentic AI challenge). The December 2024 employee stock buyback at a $2 billion valuation, 42% above the failed UBS deal, provides concrete evidence that private market investors see continued upside potential. How solid this is will only be determined by the actual market when real money is on the line.

For IPO investors, the fundamental question isn't whether Wealthfront can grow, with $80 billion in total assets, 1 million clients, and $100 million projected free cash flow, growth and scale are proven. The question is whether public markets will value this comprehensive financial platform at a premium to the $2 billion private valuation, and what they expect the disruption of all robo-advisors will be, how soon, and whether Wealthfront can adapt to the Agentic era.

Given the combination of strong fundamentals, industry recognition, and positioning in the growing direct indexing market (projected to reach $825 billion by 2026), an IPO valuation above $2 billion appears achievable, assuming the market is overlooking the existential threat posed by the Agentic era. The IPO will provide the transparency needed to determine just how much higher public investors are willing to pay for this fintech comeback story and Wealthfront`s potential to execute on its original `self-drivng`money visio,n but in the Agentic era.

The Investment Thesis Balance

Wealthfront presents a rare combination of proven fintech fundamentals and existential transformation risk. The company has successfully executed a remarkable turnaround, achieving scale, profitability, and market recognition. However, the looming agentic AI revolution poses questions that traditional financial metrics cannot answer. IPO investors must weigh strong current performance against the uncertainty of whether Wealthfront can reinvent "self-driving money" for the AI era, or become obsolete in the process.

Enjoyed this analysis and didn't realize how Betterment has fallen behind!