Is Robinhood Positioning to Capture the Generational Wealth Transfer?

A Semantic analysis of the insights of a US financial planner and Fintecher Simon Taylor on Robinhood`s positioning

A US financial planner and a Fintecher share their insights on Robinhood`s positioning: Cody Garrett`s LinkedIn Post and Simon Taylor`s Linkedin post

Simon Taylor expands the scope of the Robinhood conversation from Cody Garret`s framing “Can Robinhood compete with traditional advisors?”(a financial planner) to “Can Robinhood redefine what wealth management means in the AI age?”

Simon Taylor brings a macro, strategic lens—with both enthusiastic support and credible skepticism in the comments—that elevates Robinhood’s positioning from a discount platform to a tech-first challenger bank for the next generation of wealth.

His LinkedIn post adds several important new insights and layers to the broader Robinhood narrative that go beyond what Cody Garrett’s post and its comments covered. To be fair, Cody Garrett’s post is exclusively focused on Robinhood`s positioning solely on the advisory space.

Grab the popcorn for the small data analysis of the two linkedin posts and the comparison.

Here's a breakdown of the additional perspective Simon brings—and how it builds on or challenges earlier observations:

1 Broader Strategic Ambition: "Full-Stack Financial Superapp“

New Insight from Simon: Robinhood isn’t just offering low-fee investment management—it’s aiming to recreate the entire private banking experience through a mobile-first, AI-powered platform (e.g., CPA access, estate planning, premium perks, international transfers).

Why it matters: While Cody’s post focused on the investment advisory angle and staff turnover, Simon paints a much bigger picture—Robinhood is no longer competing with robo-advisors or financial planners. It’s going after Schwab, JPMorgan, and Morgan Stanley by building a platform that blends banking, investing, and lifestyle.

2 AI Agents as Differentiators

New Insight from Simon: Robinhood is introducing three context-aware AI agents to provide personalized advice and support across investing, research, and banking—targeting not just retail investors, but the mass-affluent who’ve traditionally relied on human advisors.

Why it matters: Cody’s post and its comments questioned the quality of Robinhood’s advisory services and staff turnover. Simon’s view reframes the conversation: it's not about scaling human advisors—it’s about replacing or augmenting them with AI. This is a conceptual leap.

3 X1 Acquisition as a Strategic Masterstroke

New Insight from Simon: Robinhood’s $90M acquisition of the X1 credit card team is presented as a core enabler of its banking strategy—not just an isolated product bet.

Why it matters: Cody’s analysis made no mention of this. Simon reveals Robinhood's growing product flywheel, connecting investments, credit, taxes, and perks—suggesting the tech infrastructure and roadmap are already maturing behind the scenes.

4 Bigger Threat Framing: Wealth Transfer & Incumbent Lag

New Insight from Simon: He links Robinhood’s strategy directly to the upcoming millennial wealth transfer and the growing frustration with legacy banks’ slow digital progress.

Why it matters: While Cody’s post focused more narrowly on industry pricing and advisor dynamics, Simon’s narrative casts Robinhood as a generational platform shift—meeting digitally-native expectations in ways incumbents can’t.

5 More Pushback on Ethics & Scale

From the Comments: Simon’s post triggered deeper discussion on regulatory risk, data privacy, and unmet human needs in wealth management. Several voices pointed out that wealth isn’t just about automation—it’s also about trust, relationships, and nuanced planning.

Why it matters: Cody’s thread focused on practical concerns (e.g. staff turnover, pricing). Simon’s post surfaces existential debates—what makes a good advisor, how AI should be governed, and what “democratizing finance” really means.

Simon Taylor - Can Robinhood Redefine Wealth Management in the Age of AI?

When Robinhood announced its new investment management product earlier this year—a 0.25% fee capped at $250 annually—the conversation quickly turned to comparisons with robo-advisors. Financial planner Cody Garrett, CFP®, noted that while Robinhood is undercutting the market on price, it still lacks financial planning and suffers from high advisor turnover. The sentiment among many professionals was cautious: impressive pricing, unclear execution.

But that cautious tone was upended when fintech commentator Simon Taylor spotlighted Robinhood's bigger ambitions in a viral LinkedIn post. According to Taylor, Robinhood isn't just chasing Vanguard or Betterment. It's gunning for Morgan Stanley and UBS.

The centerpiece? Robinhood Banking — a new service bundling real-time net worth tracking, integrated estate planning, CPA access, family accounts, and international money movement. Most provocatively, Robinhood also introduced three AI "agents" designed to provide contextual investment advice, research support, and digital private banking for the masses.

Taylor framed this as a potential "Kodak moment" for traditional private banks: while they cling to quarterly statements and wood-paneled offices, Robinhood is offering instant access, sleek design, and always-on AI support. In a world where millennials are inheriting trillions and expect Netflix-style user experiences, the pitch is compelling.

Yet questions abound. Can AI replicate the nuanced trust of a human advisor? Will affluent clients accept tax and estate advice from a chatbot? And how can Robinhood overcome its checkered history with compliance, customer service, and the infamous GameStop saga?

The responses to Taylor's post highlight the fault lines. Some call it disruptive and overdue; others see marketing hype and regulatory risk. Critics argue that estate planning and legacy conversations can’t be automated. Supporters counter that traditional private banking underserves the tech-savvy mass affluent who value control over conversation.

Interestingly, while Garrett focused on pricing transparency and advisor credibility, Taylor highlighted product integration, experience design, and brand storytelling. Their perspectives don’t conflict so much as complement: Garrett frames Robinhood as an upstart robo; Taylor sees a platform play targeting the next generation of wealth.

The bigger insight? Robinhood may not need to "replace" private banking to succeed. If it can retain its core customer base as they build wealth—and offer just enough tools, advice, and cachet along the way—it could carve out a powerful new middle ground.

In the end, the question is less about whether Robinhood can become UBS, and more about whether it can redefine what wealth management even means.

The verdict is still out. But the game has undeniably changed.

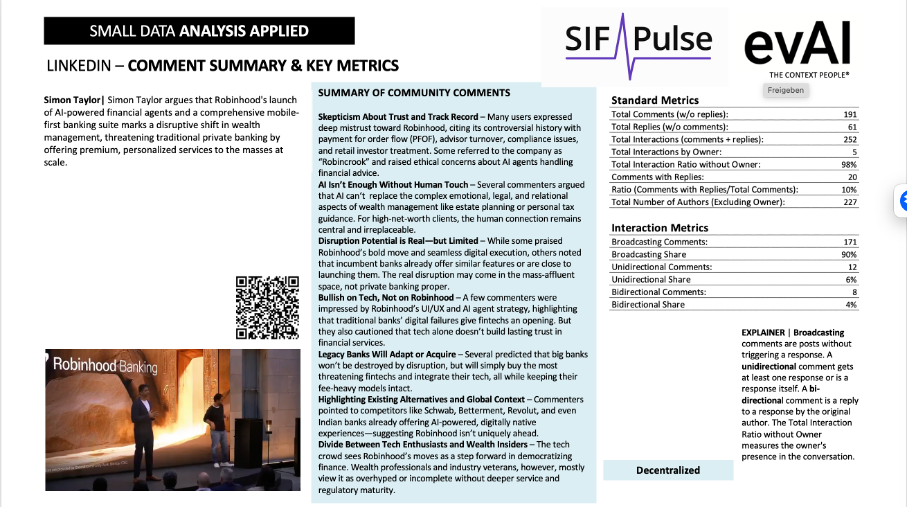

Comment Analysis

Skepticism About Trust and Track Record

– Many users expressed deep mistrust toward Robinhood, citing its controversial history with payment for order flow (PFOF), advisor turnover, compliance issues, and retail investor treatment. Some referred to the company as “Robincrook” and raised ethical concerns about AI agents handling financial advice.

AI Isn’t Enough Without Human Touch

– Several commenters argued that AI can't replace the complex emotional, legal, and relational aspects of wealth management like estate planning or personal tax guidance. For high-net-worth clients, the human connection remains central and irreplaceable.

Disruption Potential is Real—but Limited

– While some praised Robinhood’s bold move and seamless digital execution, others noted that incumbent banks already offer similar features or are close to launching them. The real disruption may come in the mass-affluent space, not private banking proper.

Bullish on Tech, Not on Robinhood

– A few commenters were impressed by Robinhood’s UI/UX and AI agent strategy, highlighting that traditional banks’ digital failures give fintechs an opening. But they also cautioned that tech alone doesn’t build lasting trust in financial services.

Legacy Banks Will Adapt or Acquire

– Several predicted that big banks won’t be destroyed by disruption, but will simply buy the most threatening fintechs and integrate their tech, all while keeping their fee-heavy models intact.

Highlighting Existing Alternatives and Global Context

– Commenters pointed to competitors like Schwab, Betterment, Revolut, and even Indian banks already offering AI-powered, digitally native experiences—suggesting Robinhood isn’t uniquely ahead.

Divide Between Tech Enthusiasts and Wealth Insiders

– The tech crowd sees Robinhood’s moves as a step forward in democratizing finance. Wealth professionals and industry veterans, however, mostly view it as overhyped or incomplete without deeper service and regulatory maturity.

I loved the analysis of the comments showing distrust in Robinhood! It made me laugh.

Robinhood has such a bad history of client care that it still amazes me that they are in business.

I don't argue that they deserve a shot at reinventing wealth management, but do any of us believe they will put the client first? I think it more likely that they will continue to strip out every penny of digital revenue from their clients no matter how abusive.